Theory and Decision ( IF 0.9 ) Pub Date : 2022-10-04 , DOI: 10.1007/s11238-022-09911-x James K. Hammitt

|

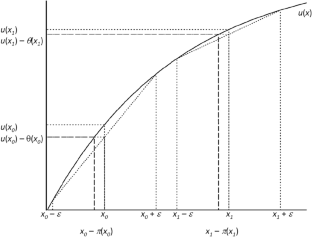

Downside risk aversion (downside RA) and decreasing absolute risk aversion (DARA) are different concepts that describe preferences for which the harm from bearing risk is lessened by an increase in wealth. This note presents some intuitive explanations of the difference between the two concepts using simple lotteries and graphical analysis. All risk-averse utility functions exhibit downside risk aversion, except those that exhibit sufficiently strong increasing absolute risk aversion. In a sense, downside RA is to be expected: adding downside risk to a baseline lottery is analogous to increasing risk while adding upside risk is analogous to decreasing risk. The difference between the two concepts can be attributed to the use of different measures of the harm from risk bearing: downside RA measures harm using the utility premium and DARA measures harm using the risk premium. The two premia can change at different rates and even in different directions as wealth increases.

中文翻译:

下行风险厌恶与降低绝对风险厌恶:直观的阐述

下行风险厌恶(下行 RA)和减少绝对风险厌恶(DARA)是描述偏好的不同概念,对于这些偏好,承担风险的伤害会因财富的增加而减少。本说明使用简单的彩票和图形分析对这两个概念之间的差异进行了一些直观的解释。所有风险厌恶效用函数都表现出下行风险厌恶,除了那些表现出足够强的增加绝对风险厌恶的函数。从某种意义上说,下行 RA 是可以预料的:在基线彩票中增加下行风险类似于增加风险,而增加上行风险类似于降低风险。这两个概念之间的差异可归因于使用不同的风险承担伤害衡量标准:下行 RA 使用效用溢价衡量损害,DARA 使用风险溢价衡量损害。随着财富的增加,这两种溢价可以以不同的速度甚至不同的方向变化。

京公网安备 11010802027423号

京公网安备 11010802027423号