Applied Mathematics and Optimization ( IF 1.6 ) Pub Date : 2022-06-07 , DOI: 10.1007/s00245-022-09838-3 Thomas Nanfeng Li 1 , Andrew Papanicolaou 2

|

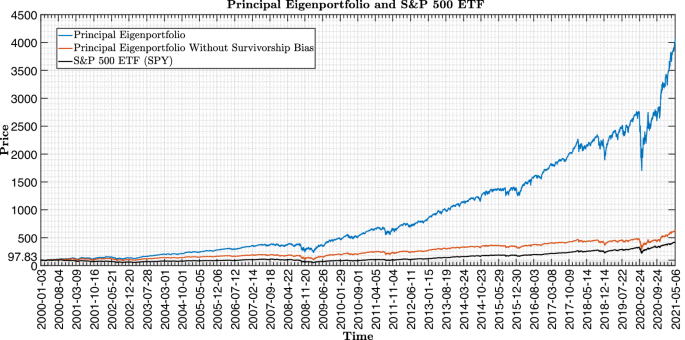

In this article, we analyse optimal statistical arbitrage strategies from stochastic control and optimisation problems for multiple co-integrated stocks with eigenportfolios being factors. Optimal portfolio weights are found by solving a Hamilton–Jacobi–Bellman (HJB) partial differential equation, which we solve for both an unconstrained portfolio and a portfolio constrained to be market neutral. Our analyses demonstrate sufficient conditions on the model parameters to ensure long-term stability of the HJB solutions and stable growth rates for the optimal portfolios. To gauge how these optimal portfolios behave in practice, we perform backtests on historical stock prices of the S&P 500 constituents from year 2000 through year 2021. These backtests suggest three key conclusions: that the proposed co-integrated model with eigenportfolios being factors can generate a large number of co-integrated stocks over a long time horizon, that the optimal portfolios are sensitive to parameter estimation, and that the statistical arbitrage strategies are more profitable in periods when overall market volatilities are high.

中文翻译:

多种联合整合股票的统计套利

在本文中,我们从随机控制和优化问题中分析了以特征组合为因素的多个协整股票的最优统计套利策略。通过求解 Hamilton-Jacobi-Bellman (HJB) 偏微分方程找到最优投资组合权重,我们求解无约束投资组合和约束为市场中性的投资组合。我们的分析证明了模型参数的充分条件,以确保 HJB 解决方案的长期稳定性和最优投资组合的稳定增长率。为了衡量这些最佳投资组合在实践中的表现,我们对标准普尔 500 指数成分股从 2000 年到 2021 年的历史股价进行了回测。这些回测得出了三个关键结论:

京公网安备 11010802027423号

京公网安备 11010802027423号